Study on Gold reserve

Dániel Palotai - István Veres

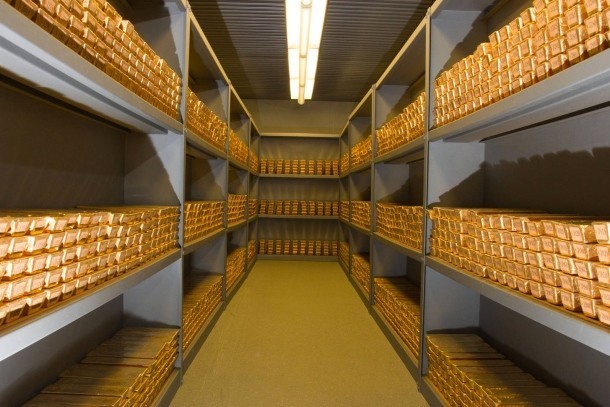

The Hungarian National Bank (MNB) began its steps to secure and increase the country’s gold reserves in 2018. This year, the central bank first repatriated the country’s reserves held abroad and then increased their volume by nearly tenfold. Six years later, in 2024, the MNB made another purchase, thanks to which the domestic gold reserves expanded to an unprecedented level, even in historical terms, by 110 tons.

The Monetary Council of the Hungarian National Bank (MNB) has taken a historic decision to review its gold reserve policy, taking into account the country’s long-term national and economic strategic goals. As a result, the central bank first moved its gold reserves from London to storage locations in Hungary in March 2018, increasing its total stock tenfold by October 2018, tripling it again by 2021, and increasing it further in 2024. The gold stock increased from 3.1 tons to 31.5 tons, then to 94.5 tons, and then to 110 tons.

The move, which represents a return to the historical roots of central banking activity, is justified by two factors. According to the central bank side of the question, the MNB must hold one of the world's safest assets in its foreign exchange reserves, which also has good diversification properties and a liquid market. The public finance side is just as important. Following the difficult years of the global financial crisis, which undermined confidence in the financial system as a whole and fundamentally transformed the attitude of central banks to gold, Hungary needed a credible instrument that could strengthen stability and confidence even under normal market conditions, symbolizing strength and wealth.

The Hungarian National Bank believes that the gold reserves held in the country not only serve as a line of defence in times of extreme market conditions but also strengthen confidence. Ownership of gold therefore serves not only investment but also economic strategic considerations.

Foreign exchange reserve management considerations

Gold is a traditional reserve asset that fits well into the conservative reserve management framework of central banks. The primary purpose of holding foreign exchange reserves is to ensure monetary policy and financial stability, so when a central bank is forced to choose between safety, liquidity and yield, it typically chooses safety and liquidity over yield.

In terms of safety, one of the most important characteristics of gold is that it has no risk of default. The foreign exchange reserves of central banks are predominantly made up of fixed-interest instruments, mainly high-rated, short-term government securities, supranational and agency bonds. These are the instruments that pose the lowest possible credit risk to the investor in the investment portfolio. However, they also represent the debt of the issuers, whose solvency or willingness to pay may become doubtful in extreme circumstances. Gold is not like that: gold does not represent any obligation of anyone, so it can be considered a truly bankruptcy-free financial instrument.

Gold is also an extremely liquid asset. In terms of market size, transaction costs and daily turnover, the gold market is comparable to other major market segments. The daily turnover of the gold market has previously been estimated at around $250 billion. During the market turbulence that took place in March 2020, gold, like other asset classes, experienced significant position liquidation and a consequent price drop. However, analyses have shown that during turbulence, gold served as a source of liquidity, i.e. investors obtained the funds necessary to meet their deposit obligations related to other asset classes by selling gold. In addition to its liquid market, gold has little correlation with the price movements of other asset classes, therefore it has favourable diversification characteristics in traditional reserve portfolios.

Building Trust

“In extreme cases, no one accepts paper money. Gold is always accepted,” Alan Greenspan, chairman of the Federal Reserve, told the House Banking Committee in 1999. Gold builds trust and enhances economic stability. This is true under normal circumstances, but it is especially true during extreme market conditions, crises, or periods of significant geopolitical uncertainty, when economic strategic considerations and the safe haven role of gold become more important.

Gold, especially in physical form, is an asset that can build trust in a country both within and outside its borders. One of the most important changes in central bank behaviour after the global financial crisis was the need to store gold domestically rather than in distant financial centres. Central banks have been announcing repatriation programs one after another. In addition to extreme market conditions, global geopolitical uncertainties also make gold availability and the benefits of domestic storage versus foreign storage a significant consideration. The vast difference between the two is obvious.

Historical ties

According to examples from Hungarian history, the country has always had a special relationship with gold. The Carpathian Basin has been surrounded by rich gold deposits since ancient times. Archaeological finds prove that goldsmithing appeared in the region as early as the Early Bronze Age, and the rich gold mines also encouraged the Roman Empire to conquer and occupy the area.

In the Middle Ages, between the 13th and 15th centuries, Hungary was the largest gold producer in Europe for about three hundred years. At that time, Hungary produced 25 percent of the world's gold and 20 percent of its silver. In European comparison, the figures are even more significant: in its heyday, the Kingdom of Hungary produced about 80 percent of the continent's total gold production, with an annual output of 2,500 kg. Besides Hungary, another significant producer was Bohemia, and then, behind it, the Holy Roman Empire, thanks to the gold deposits in the Rhine Valley. Hungary maintained its leading position in the extraction of precious metals until the discovery of the American continent and the Turkish occupation of the country.

At that time, several types of gold coins were in circulation in Europe, of which the Venetian gold ducat was the most famous. However, other, progressive regions also produced their own coins, including King Charles Robert of Hungary in 1325. These coins, which were of similar weight and purity to the Venetian ducat, were also widely accepted as currency throughout Europe. Hungary minted ducats until 1915.

Gold in danger

The MNB has been holding gold reserves since its founding in 1924. During the stabilization period following World War I (1924-29), the stock grew rapidly, and the value of the new currency, the pengő, was pegged to gold in 1927. The largest reserve stock, about 53 tons, was formed before the Great Depression and remained stable until World War II.

The Hungarian central bankers personally protected the domestic gold reserves. Perhaps the tensest period in the lives of the Hungarian central bankers came in the last months of the war, when about 400 volunteers from among the central bank employees managed to save the Hungarian national treasures from the occupying forces. These volunteers accompanied the so-called gold train carrying the 30-ton gold stock, melted into 25-kg ingots, and the entire pengő banknote stock. The estimated value of the shipment at the time was around $1 billion. The train left the capital in November 1944 and arrived in the Austrian town of Spital am Pyhrn in January 1945, where the shipment was guarded by central bank employees until American troops led by General George Patton arrived in May 1945.

After the war, in August 1946, the shipment – including the 30 tons of gold reserves – returned to Hungary intact. This was a rare occurrence at the time. These 30 tons of gold were one of the main pillars of the post-war economic and financial consolidation and were used to introduce the new currency, the forint.

Saving the gold reserve – the story of the MNB gold train

The excellent staff of the Hungarian National Bank saved the country’s gold reserves from the devastation of war by demonstrating extraordinary courage in difficult circumstances and thus deserved the respect of posterity.

Learn about the story of the MNB gold train!

Years of active management

Like all other elements of the foreign exchange reserves, gold reserves were actively managed. This was also the case in the 1970s and 1980s, when the MNB resumed publishing data on reserves after a complete silence of about two decades. Unfortunately, very little information is available from the times before the change of regime. The available data shows that the level of gold reserves peaked at around 70-80 tons, and that sales and purchases were mainly based on price developments and exchange rate expectations.

Later, active management of gold reserves was based on yield considerations. Until 2018, the MNB held the gold in an unallocated form in London, with international depositories, and used all available tools to increase the available yield. Depending on market conditions, the central bank either did not invest, placed the gold reserves with its partners for a short term or taking advantage of occasional arbitrage opportunities, exchanged the gold for another currency and placed the proceeds in money market instruments. These investments resulted in overall returns exceeding storage costs.

Business Outcome

The Monetary Council of the MNB continuously monitors gold market developments and decides accordingly on all possible aspects of gold reserve management. The gold reserve serving national strategic objectives was not sold, its size increased to 110 tons by 2024 and is kept in physical form in a domestic storage facility.